General Laws of Massachusetts - Chapter 65 Taxation of Legacies and Successions - Section 1 Subjects of taxation; rates; exceptions

Section 1. All property within the jurisdiction of the commonwealth, corporeal or incorporeal, and any interest therein, belonging to inhabitants of the commonwealth, and all real estate or any interest therein and all tangible personal property within the commonwealth belonging to persons who are not inhabitants of the commonwealth, except such an interest in such real estate as is represented by a mortgage or by a transferable certificate of participation or share of an association, partnership or trust, which shall pass by will, or by laws regulating intestate succession, or by deed, grant or gift, except in cases of a bona fide purchase for full consideration in money or money’s worth, made in contemplation of the death of the grantor or donor or made or intended to take effect in possession or enjoyment after his death, and any beneficial interest

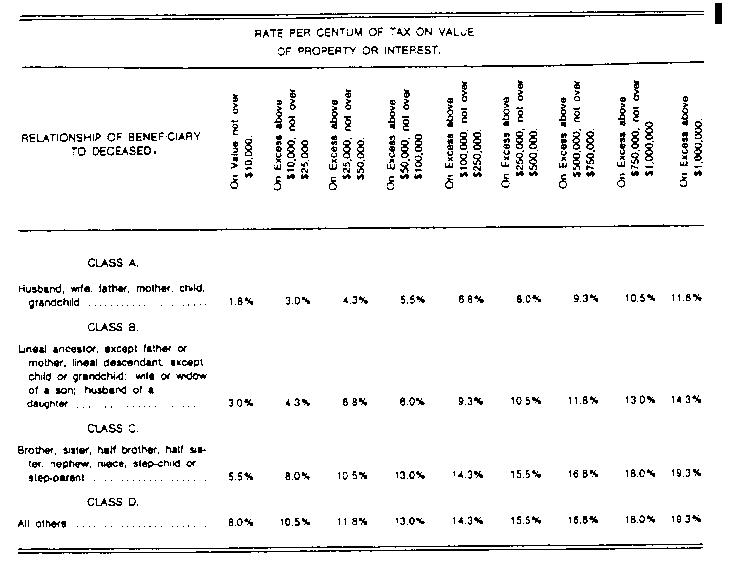

therein which shall arise or accrue by survivorship in any form of joint ownership, or in any tenancy by the entirety in which the decedent contributed during his life any part of the property held in such joint ownership or tenancy by the entirety or of the purchase price thereof and proceeds of insurance receivable under policies of the life of the decedent, to any person, absolutely or in trust, except (1) to or for the use of charitable, educational or religious societies or institutions which are organized under the laws of, or charitable, educational or religious societies or institutions, incorporated or unincorporated, whose principal charitable, educational or religious objects are solely carried out within, or whose charitable, educational or religious objects are principally and usually carried out within, or whose charitable, educational or religious activities are principally and usually carried out within the commonwealth; or which are organized under the laws of, or whose principal charitable, educational or religious objects are carried out within any other state or states of the United States which exempt from similar taxation legacies and devises by its citizens to or for the use of such societies or institutions which are organized under the laws of, or whose principal charitable, educational or religious objects are carried out within the commonwealth; or (2) for the saying, singing, performance or celebration of religious rites, rituals, services or ceremonies whether to be conducted within or without the commonwealth; or (3) for or upon trust for any charitable purposes to be carried out within the commonwealth and/or within any other state or states of the United States which exempt from similar taxation legacies and devises by its citizens for charitable purposes to be carried out within this commonwealth; or (4) to or for the use of the commonwealth or any town therein for public purposes; or (5) any payment made from the retirement funds of the federal government to a spouse, child or other dependent of the decedent as a result of his death, shall be subject to a tax at the percentage rates fixed by the following table:—

Provided, however, that in the case of any beneficial interest arising or accruing by survivorship of a husband or wife in a tenancy by the entirety or joint tenancy in single family residential property occupied by such husband and wife as a domicile, there shall be allowed an exemption of such property to the extent of its value, and in multiple family residential property so occupied there shall be allowed an exemption of such property to the extent of twenty-five thousand dollars of its value.

Provided, however, that no property or interest therein, which shall pass or accrue to or for the use of a husband or wife unless its value exceeds thirty thousand dollars or to or for the use of any other person in Class A unless its value exceeds fifteen thousand dollars, and no other property or interest therein unless its value exceeds five thousand dollars shall be subject to the tax imposed by this chapter, and no tax shall be exacted upon any property or interest so passing or accruing which shall reduce the value of such property or interest below said amounts; provided, however, that no amounts attributable to employer contributions payable under a retirement plan which meets the requirements of section four hundred and one or section four hundred and three of the federal Internal Revenue Code, except amounts payable to the employee’s executors, shall be subject to the tax imposed by this section.

Provided, however, that proceeds of insurance receivable under policies on the life of the decedent shall be subject to the tax imposed by this chapter to the extent of (1) the amounts receivable by the executor or administrator of the estate of the decedent and (2) the amounts receivable by all other beneficiaries under policies with respect to which the decedent possessed at his death any incidents of ownership, exercisable either alone or in conjunction with any other person, within the meaning of section two thousand forty-two of the Federal Internal Revenue Code, as amended and in effect at the date of death of the decedent; and provided, further, that twenty-five thousand dollars of the proceeds receivable as named beneficiaries under said policies by a surviving husband, wife or issue, or any combination of the foregoing, or by trustees of intervivos trusts for their benefit shall be exempt from tax; and if the proceeds receivable by such persons and such trustees exceed twenty-five thousand dollars, the exemption shall first apply to proceeds receivable by the surviving husband or wife, secondly, to the proceeds receivable by the surviving issue, allocated among them in proportion to the amounts receivable by each, thirdly to the proceeds receivable by the trustees for the benefit of the surviving husband or wife and fourthly to the proceeds receivable by trustees for the benefit of issue.

All property and interests therein which shall pass from a decedent to the same beneficiary by any one or more of the methods hereinbefore specified and all beneficial interests which shall accrue in the manner hereinbefore provided to such beneficiary on account of the death of such decedent shall be united and treated as a single interest for the purpose of determining the tax hereunder.

For the purposes of this section, a person adopted in accordance with chapter two hundred and ten, or a person adopted in another state or country in accordance with the laws thereof, his adoptive ancestors and adoptive descendants, both lineal and collateral, shall stand in the same relationship to the deceased as if the person adopted had been born to his adoptive parent in lawful wedlock.

Section: 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 NextLast modified: September 11, 2015